Market Matters – Musical Chairs for UK PM

UK Politics: Keir Starmer’s resignation has pushed UK politics back to the front of investors’ minds, with Andy Burnham looking the clear favourite to take over. This is not an ideal backdrop. The UK still suffers from political instability, a heavy fiscal burden and a policy mix that often seems to repel the capital it says it wants to attract.

The biggest change has been the fall in oil prices following the easing of tensions around Iran and the Strait of Hormuz. The recent energy shock had threatened to push inflation expectations higher and force the Bank of England into a more hawkish stance. Instead, inflation expectations have eased, gilt yields have come off their highs, and markets have begun to price out more aggressive rate-rise scenarios. This gives a new Prime Minister some room for manoeuvre. It does not solve the UK’s deeper problems: weak growth, stretched public finances and a high tax burden. Nor does it remove the risk that a Burnham administration funds higher public spending through more borrowing, higher taxes or creative off-balance-sheet structures. But the immediate market backdrop is less hostile than it might have been.

For investors, the question is whether the UK is now so unloved that much of the bad news is already reflected in prices. Over the past decade, the S&P 500 has delivered a total return of more than 340% in sterling terms, while the FTSE 100 is up around 150%, the FTSE 250 around 90% and UK smaller companies just over 80%. The domestic political backdrop remains messy, but many UK-listed companies are not purely UK businesses. A large part of FTSE 100 revenues comes from overseas, and even the mid- and small-cap universe contains companies with international earnings streams. The UK is not a screaming buy, but it does argue for selective exposure to companies listed in the UK that are not overly dependent on the UK economy.

Hormuz’s Fragile Peace: The more constructive UK and European inflation backdrop still rests heavily on one assumption: that the fall in energy prices sticks. The latest news from the Strait of Hormuz is a reminder that this remains a fragile assumption. The US and Iran have now exchanged fresh attacks, with commercial vessels targeted, US strikes on Iranian military infrastructure and Iran reportedly launching missiles and drones at US-linked bases in Kuwait and Bahrain.

For markets, the important point is not simply the military exchange itself, but what it says about the ceasefire. This now looks less like a settled truce and more like a heavily strained pause in a wider conflict. Shipping through Hormuz continues, but maritime security warnings have increased, mine risks have been flagged, and the dispute over whether Iran can impose tolls or control arrangements in the Strait remains unresolved.

Oil has already fallen close to pre-war levels, and much of the recent improvement in the inflation-and-rates narrative depends on that move holding. Lower oil prices have helped ease inflation expectations, reduce pressure on gilt yields, and take some central bank tightening risk out of markets. If Hormuz traffic continues and Brent remains closer to $75 than to $100, that would remain supportive for growth-sensitive assets. If the situation escalates, the market would have to reprice energy, inflation and central bank risk very quickly.

So far, investors have largely looked through the geopolitical noise. That may still prove correct, but the margin for error has narrowed. Hormuz remains the key near-term geopolitical risk to the more benign inflation story.

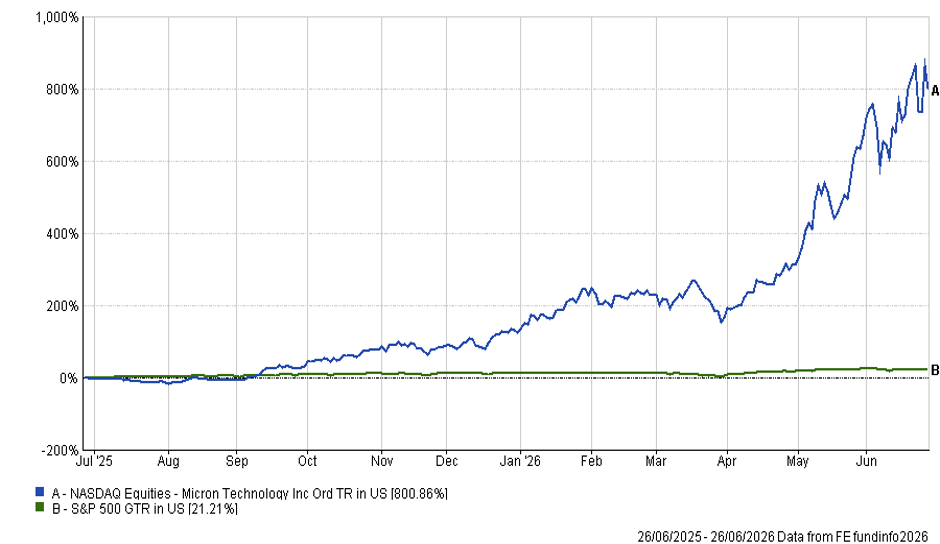

Micron: In the US, the most important corporate news came from Micron, whose results reminded investors that the AI infrastructure story is still producing real earnings. Revenue and profits were well ahead of expectations, guidance was materially stronger than forecast, and the company pointed to significant long-term customer commitments for memory chips. Despite the extraordinary share-price move, Micron’s forward P/E has barely expanded: it is still only around 9–10x forward earnings, broadly similar to a year ago, because earnings expectations have risen almost as fast as the share price.

The Micron story is really important because memory has become a key bottleneck in the AI build-out. Demand is showing up in pricing power, margins, forward contracts and capacity constraints. Micron’s results also broadened the AI story beyond Nvidia. The market has spent much of the past two years treating AI as if it were almost entirely about GPUs and the hyperscalers buying them. Micron is a reminder that memory, storage, networking, power, cooling and data-centre infrastructure are all part of the same investment cycle. The AI trade remains earnings-led rather than purely narrative-led.

Magnificent Seven: The wobble in the Magnificent Seven last week should not be dismissed. The market is no longer prepared to automatically reward every dollar of AI capital expenditure. Last week, the Magnificent Seven fell sharply while the equal-weighted S&P 500 rose.

That is probably the right way to think about the recent weakness in big tech. It does not mean the AI theme is broken. It means the market is moving from the excitement phase to the accountability phase. Investors are asking a harder question: who actually earns the return on this spending?

The suppliers of scarce components may be in a stronger position than the platforms funding the build-out. If memory, electricity, land, chips and cooling all become more expensive, the cost of staying in the AI race rises. That is manageable for the largest technology companies, but it creates more pressure on margins, free cash flow and investor patience.

US economy: The US economic data complicated the picture. Activity remains resilient: consumer spending is still growing, jobless claims remain low, and business investment is being supported by the AI infrastructure cycle.

But inflation is not yet back under control. Core PCE remains too high for comfort, and the recent improvement in headline inflation depends heavily on lower energy prices.

That leaves the Federal Reserve in a difficult position. The economy is not weak enough to force a quick pivot back to rate cuts, while inflation is still firm enough to keep the risk of another hike alive. Our view remains that further Fed tightening is unlikely, particularly if lower oil feeds through into softer inflation expectations. Markets are still pricing some risk of additional hikes this year, and we think that can be taken out if the data cooperate.

Korea and Asian technology: Asia remains central to the AI infrastructure story, but Korea’s market action was a reminder that strong fundamentals do not remove volatility risk. The KOSPI has become increasingly dominated by Samsung Electronics and SK Hynix, and recent moves have been extraordinary. Micron’s results confirmed that memory demand remains exceptionally strong, particularly in high-bandwidth memory used in AI servers. That supports the case for the Korean memory leaders.

However, the price action has become uncomfortable. The issue is not that the earnings story is weak; it is that share prices have moved quickly and the market is now reacting violently to any concern about demand, pricing or customer pushback. The planned US listing by SK Hynix adds to the sense that the market is trying to capitalise on peak enthusiasm for AI infrastructure. The company has a legitimate need to fund capacity expansion, but large capital raisings after very strong share-price moves are worth noting. They can be a sign of real opportunity, but also of a market becoming more crowded.

There is also a market-structure issue. Leveraged products linked to Samsung and SK Hynix appear to be amplifying intraday moves. Korea is already a concentrated market. When a handful of semiconductor names dominate index performance, and leveraged flows chase those same names, volatility can become self-reinforcing. Some air coming out of the market may therefore be healthy rather than alarming.

The broader Asian technology case still looks compelling. China is building out its own AI infrastructure and domestic semiconductor ecosystem, while Taiwan remains critical through TSMC. Across the region, the AI theme focuses on factories, memory, foundries, power, equipment, data centres, and supply chains. The memory upcycle appears intact, but after such strong moves, Korea may be a market where the long-term story remains attractive while the short-term trading environment is dangerous.

In summary – a continuation of the rotation, not yet a deterioration

Technology stocks, especially AI winners, continue to face pressure due to concerns about valuations, market crowding, and capital expenditures.

Equal-weighted indices, cyclical stocks, credit markets, and parts of Europe have shown more resilience, supported by falling oil prices and optimism that central banks may not need to tighten monetary policy significantly.

This aligns with our perspective over the past few weeks. While we are not negative on technology, we believe that market leadership should diversify. Markets heavily reliant on a small number of major tech companies is always at risk of derailment. In contrast, markets in which lower energy prices, robust growth, and more stable bond yields enable various sectors to thrive is clearly healthier!

This week…

The coming week brings both month-end and quarter-end, so some position squaring and profit-taking would not be surprising, particularly after such a strong run in parts of the technology sector. That may keep markets choppy in the near term. July has historically been a supportive month for equities, and we remain in the bullish camp, but the market may need to digest crowded positioning before making further progress.

The main macro focus will be the US labour market. JOLTS, ADP, jobless claims and the June payrolls report will all be watched closely. A soft but not recessionary number would probably be the most market-friendly outcome, supporting the idea that growth is cooling without breaking and that the Fed does not need to tighten again. A very strong number could revive rate-hike concerns, while a genuinely weak number would raise a different worry around growth.

Outside the US, the focus will be on eurozone inflation, the ECB’s Sintra forum, China PMIs and Japan’s Tankan survey. The other live issue is Hormuz. Markets have taken comfort from the fall in oil prices, but the latest US-Iran exchanges mean energy risk cannot be ignored. Any disruption to shipping, insurance or tanker flows would quickly challenge the recent improvement in inflation expectations.

Overall, the market is still being pulled between supportive forces — lower oil prices, resilient growth, and strong AI-related earnings — and risks around geopolitics, sticky core inflation, stretched technology positioning, and leveraged flows in Asia. We remain constructive, but not complacent. The path of least resistance for equities still looks higher into July, but the next phase should be more selective, more balanced and less dependent on the Magnificent Seven alone.